Medicare Considerations for Retiring Employees

By Brian Gilmore | Published September 1, 2017

Health benefits are one of the many issues to consider prior to retirement.

Question: What are the Medicare issues to consider for age 65+ employees who are retiring?

Compliance Team Response:

There are five key Medicare items for retirees to be aware of:

1.8-Month Special Enrollment Period

The employee will have an 8-month special enrollment period for Medicare Part A and/or Part B that starts the month after employment ends or active coverage ends—whichever happens first.

2. Avoiding Medicare Part B Penalties

COBRA coverage (unlike active coverage) does not qualify to avoid the Medicare Part B late enrollment penalty. Medicare-eligible retirees have eight months from the loss of active coverage (regardless of whether they elect COBRA) to enroll in Medicare to avoid that penalty.

3. Medicare Pays Primary for COBRA Qualified Beneficiaries

In general, the Medicare Secondary Payer (MSP) rules require that the employer-sponsored group health plan always pay primary to Medicare for individuals in “current employment status.” This means for any active employee or spouse (but not DP), Medicare will pay secondary.

However, retirees enrolled in COBRA (or an employer-sponsored plan for retirees) are not receiving employer-sponsored coverage based on “current employment status.” In other words, they are not active. This means that Medicare pays primary for anyone enrolled in COBRA.

4. COBRA Eligibility Lost Upon Medicare Enrollment After COBRA Election:

COBRA coverage can terminate early based on Medicare enrollment (not mere eligibility), but only if the Medicare enrollment occurs after the COBRA election.

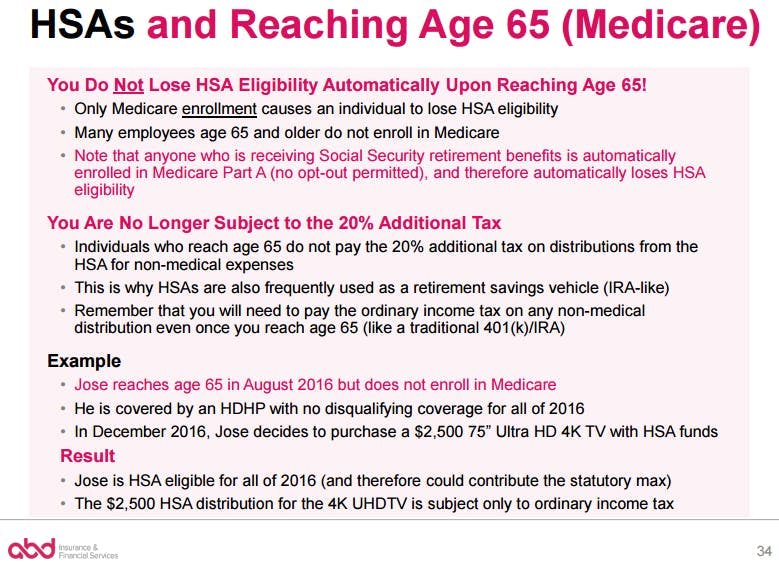

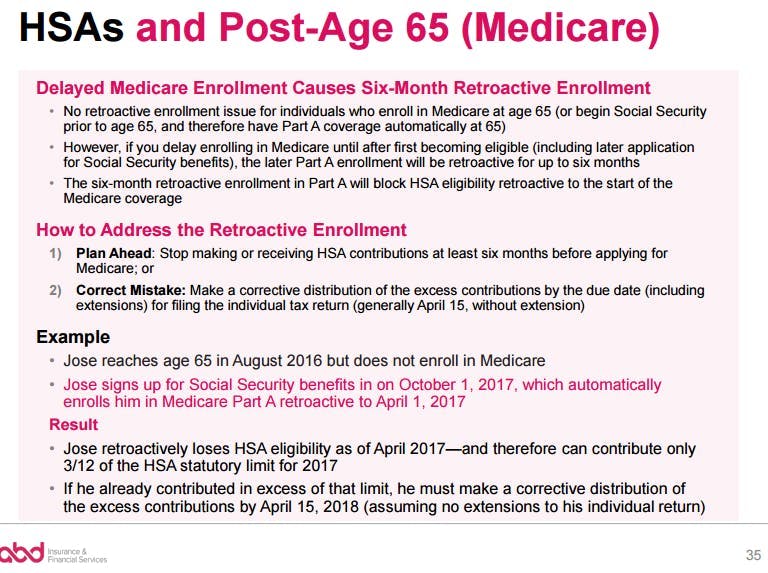

5. Medicare Enrollment Blocks HSA Eligibility

These rules are best summarized in our Newfront 'Go All the Way with HSA' guide.

We’ve copied a few relevant cites below for reference.

Regulations:

Special circumstances (Special Enrollment Periods)

Once your Initial Enrollment Period ends**,** you may have the chance to sign up for Medicare during a Special Enrollment Period. If you’re covered under a group health plan based on current employment, you have a Special Enrollment Period to sign up for Part A and/or Part B any time as long as you or your spouse (or family member if you’re disabled) is working, and you’re covered by a group health plan through the employer or union based on that work.

You also have an 8-month Special Enrollment Period to sign up for Part A and/or Part B that starts the month after the employment ends or the group health plan insurance based on current employment ends, whichever happens first. Usually, you don’t pay a late enrollment penalty if you sign up during a Special Enrollment Period.

When employer/union coverage ends

Once your employment (or your employer/union coverage) ends, 3 things happen:

You may be able to get COBRA coverage, which continues your health insurance through the employer’s plan (in most cases for only 18 months) and probably at a higher cost to you.

You have 8 months to sign up for Part B without a penalty, whether or not you choose COBRA. To sign up for Part B while you’re employed or during the 8 months after employment ends, complete an Application for Enrollment in Part B (CMS-40B) and a Request for Employment Information (CMS-L564). If you choose COBRA, don’t wait until your COBRA ends to enroll in Part B. If you don’t enroll in Part B during the 8 months after the employment ends:

You may have to pay a penalty for as long as you have Part B.

You won’t be able to enroll until January 1–March 31, and you’ll have to wait until July 1 of that year before your coverage begins. This may cause a gap in health care coverage.

If you already have COBRA coverage when you enroll in Medicare, your COBRA will probably end. If you become eligible for COBRA coverage after you’re already enrolled in Medicare, you must be allowed to take the COBRA coverage. It will always be secondary to Medicare (unless you have End-Stage Renal Disease (ESRD)).Learn more about how Medicare works with other insurance.

Treas. Reg. §54.4980B-7, Q/A-3(a):

**Q-3. ** When may a plan terminate a qualified beneficiary’s COBRA continuation coverage due to the qualified beneficiary’s entitlement to Medicare benefits?

**A-3. **(a) If a qualified beneficiary first becomes entitled to Medicare benefits under Title XVIII of the Social Security Act (42 U.S.C. 1395-1395ggg) after the date on which COBRA continuation coverage is elected for the qualified beneficiary, then the plan may terminate the qualified beneficiary’s COBRA continuation coverage upon the date on which the qualified beneficiary becomes so entitled. By contrast, if a qualified beneficiary first becomes entitled to Medicare benefits on or before the date that COBRA continuation coverage is elected, then the qualified beneficiary’s entitlement to Medicare benefits cannot be a basis for terminating the qualified beneficiary’s COBRA continuation coverage.

(b) A qualified beneficiary becomes entitled to Medicare benefits upon the effective date of enrollment in either part A or B, whichever occurs earlier. Thus, merely being eligible to enroll in Medicare does not constitute being entitled to Medicare benefits.

42 USC §1395y(b)(1)(A)(i)(l):

(b) Medicare as secondary payer.

_(1) _Requirements of group health plans.

(A) Working aged under group health plans.

(i) In general. A group health plan—

(I) may not take into account that an individual (or the individual’s spouse) who is covered under the plan by virtue of the individual’s current employment status with an employer is entitled to benefits under this subchapter under section 426(a) of this title, and

(II) shall provide that any individual age 65 or older (and the spouse age 65 or older of any individual) who has current employment status with an employer shall be entitled to the same benefits under the plan under the same conditions as any such individual (or spouse) under age 65.

HHS Letter Addressing Application of the MSP Rules to COBRA Coverage

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn