Limited Purpose Health FSA Preventive Expenses

By Brian Gilmore | Published June 29, 2018

Question: Can a limited purpose health FSA reimburse preventive medical expenses (in addition to dental and vision expenses) without affecting HSA eligibility?

Compliance Team Response:

Limited-Purpose Health FSA

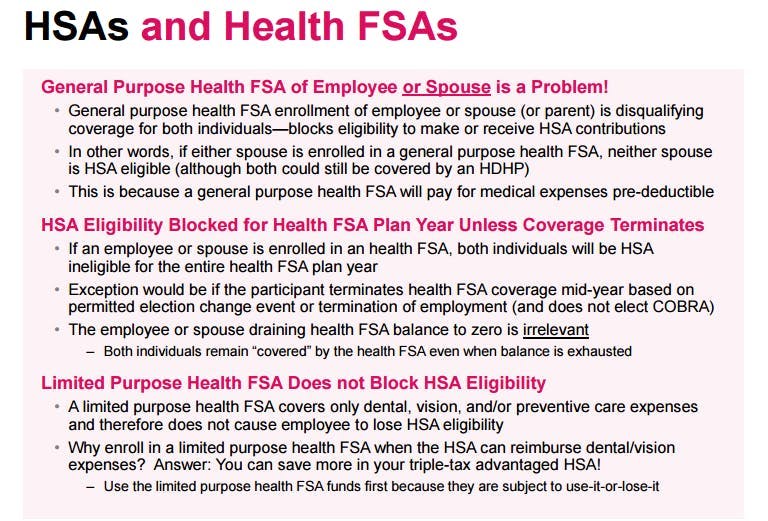

Enrollment in a limited purpose health FSA does not block HSA eligibility. It may reimburse only dental/vision/preventive expenses of the employee or a qualifying dependent.

Preventive expenses can be medical, dental, or vision. A limited purpose health FSA can reimburse preventive medical expenses because a HDHP can cover pre-deductible preventive medical expenses without cost-sharing. In other words, because the HSA rules are designed to permit a HDHP to provide first-dollar preventive medical coverage, a limited purpose health FSA can also reimburse pre-deductible preventive medical expenses without blocking HSA eligibility.

Keep in mind that the ACA requires (non-grandfathered) major medical plans to cover preventive services with no cost-sharing. This means employees frequently will not have any unreimbursed out-of-pocket preventive medical expenses to submit.

For full details on how health FSAs affect HSA eligibility, see our prior FAST: HSA Interaction with Health FSA.

Regulations:

Prop. Treas. Reg. §1.125-5(m)(3):

(m) HSA-compatible FSAs-limited-purpose health FSAs and post-deductible health FSAs.

(1) In general. Limited-purpose health FSAs and post-deductible health FSAs which satisfy all the requirements of section 125 are permitted to be offered through a cafeteria plan.

(2) HSA-compatible FSAs. Section 223(a) allows a deduction for certain contributions to a “Health Savings Account” (HSA) (as defined in section 223(d)). An eligible individual (as defined in section 223(c)(1)) may contribute to an HSA. An eligible individual must be covered under a “high deductible health plan” (HDHP) and not, while covered under an HDHP, under any health plan which is not an HDHP. A general purpose health FSA is not an HDHP and an individual covered by a general purpose health FSA is not eligible to contribute to an HSA. However, an individual covered by an HDHP (and who otherwise satisfies section 223(c)(1)) does not fail to be an eligible individual merely because the individual is also covered by a limited-purpose health FSA or post-deductible health FSA (as defined in this paragraph (m)) or a combination of a limited-purpose health FSA and a post-deductible health FSA.

(3) Limited-purpose health FSA. A limited-purpose health FSA is a health FSA described in the cafeteria plan that only pays or reimburses permitted coverage benefits (as defined in section 223(c)(2)(C)), such as vision care, dental care or preventive care (as defined for purposes of section 223(c)(2)(C)). See paragraph (k) in this section.

IRC §223(c)(2)(C):

(C) Safe harbor for absence of preventive care deductible. A plan shall not fail to be treated as a high deductible health plan by reason of failing to have a deductible for preventive care (within the meaning of section 1861 of the Social Security Act, except as otherwise provided by the Secretary).

Newfront Office Hours: Go All the Way with HSA

HSAs and Health FSAs

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn