Early Termination of COBRA Upon Enrollment in Other Group Health Plan or Medicare

By Brian Gilmore | Published November 1, 2019

**Question: **How does enrollment in another employer-sponsored group health plan or Medicare affect a qualified beneficiary’s COBRA rights?

Compliance Team Response:

-

**Short Answer: **COBRA generally terminates early where the qualified beneficiary first becomes covered under another group health plan or Medicare after COBRA is elected.

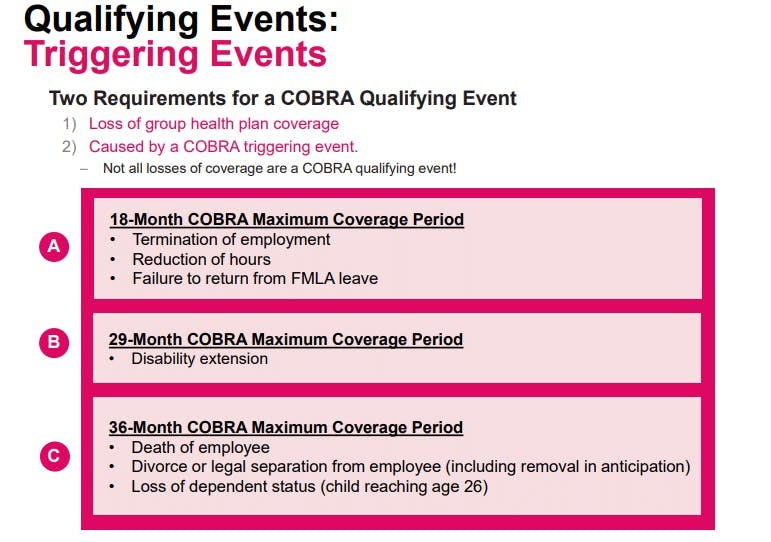

General Rule: COBRA Maximum Coverage Period

Absent an early termination event, the COBRA maximum coverage period is as follows:

18 Months:

Termination of employment

Reduction of hours

Failure to return from FMLA leave

29 Months:

Disability extension

36 Months:

Death of employee

Divorce or legal separation from employee

Child reaches age 26

As described below, certain events can cause the qualified beneficiary to lose COBRA rights prior to the end of the maximum coverage period.

Early Termination of COBRA Upon Enrollment in Another Group Health Plan

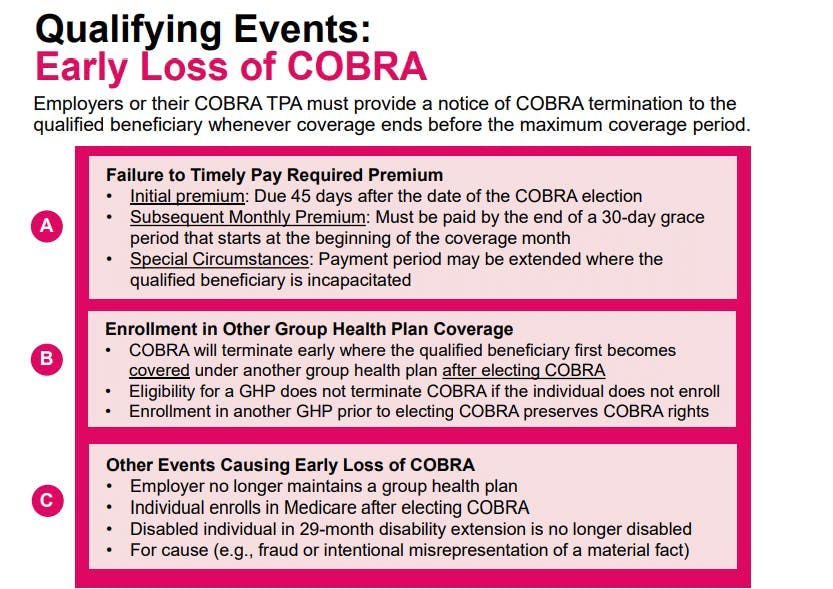

COBRA can terminate early if the qualified beneficiary first becomes covered under another group health plan after electing COBRA.

There are a few key points with this rule:

Mere eligibility for another group health plan does not affect COBRA rights.

The individual must actually enroll and become covered under the other group health plan to cause early termination.

The enrollment in the other group health plan must occur after the qualified beneficiary elected COBRA to cause early termination.

The timing piece means that a qualified beneficiary who enrolled in another group health plan prior to electing COBRA will not be subject to early termination of COBRA because of that other group health plan enrollment. In other words, qualified beneficiaries who want to have other group health plan coverage and remain on COBRA must be careful to enroll in the other group health plan prior to electing COBRA.

This timing rule stems from the 1998 U.S. Supreme Court case Geissal v. Moore Med. Corp., which is the only U.S. Supreme Court case to address COBRA rights. Since the U.S. Supreme Court’s ruling, the IRS has updated the COBRA regulations to confirm that only enrollment in another group health plan after electing COBRA can cut short the qualified beneficiary’s COBRA rights (Treas. Reg. §54.4980B-7, Q/A-2).

Early Termination of COBRA Upon Enrollment in Medicare

COBRA can also terminate early if the qualified beneficiary enrolls in Medicare after electing COBRA.

There are a few key points with this rule:

Mere eligibility for Medicare (e.g., reaching age 65) does not affect COBRA rights.

Although the COBRA rules refer to Medicare “entitlement,” guidance confirms that “entitlement” means “enrollment.”

The enrollment in Medicare must occur after the qualified beneficiary elected COBRA to cause early termination.

The timing piece means that a qualified beneficiary who enrolled in Medicare prior to electing COBRA will not be subject to early termination of COBRA because of the Medicare enrollment. In other words, qualified beneficiaries who want to have Medicare and remain on COBRA must be careful to enroll in Medicare prior to electing COBRA.

This timing rule stems from the 1998 U.S. Supreme Court case Geissal v. Moore Med. Corp., which is the only U.S. Supreme Court case to address COBRA rights. Since the U.S. Supreme Court’s ruling, the IRS has updated the COBRA regulations to confirm that only enrollment in Medicare after electing COBRA can cut short the qualified beneficiary’s COBRA rights (Treas. Reg. §54.4980B-7, Q/A-3).

Other Early Termination of COBRA Events

COBRA qualified beneficiaries can also have their COBRA rights terminated prior to exhausting the maximum coverage period for the following reasons:

Failure to timely pay the required initial COBRA premium within 45 days of the COBRA election;

Failure to timely pay the subsequent monthly COBRA premium by the end of a 30-day grace period that starts at the beginning of the coverage month;

Where the employer no longer maintains a group health plan;

Where the qualified beneficiary is no longer disabled during the 29-month disability extension period; or

For cause, such as the qualified beneficiary committing fraud or intentionally misrepresentation of a material fact.

Regulations

Treas. Reg. §54.4980B-7, Q/A-2:

**Q-2. ** When may a plan terminate a qualified beneficiary’s COBRA continuation coverage due to coverage under another group health plan?

**A-2. **(a) If a qualified beneficiary first becomes covered under another group health plan (including for this purpose any group health plan of a governmental employer or employee organization) after the date on which COBRA continuation coverage is elected for the qualified beneficiary and the other coverage satisfies the requirements of paragraphs (b), (c), and (d) of this Q&A-2, then the plan may terminate the qualified beneficiary’s COBRA continuation coverage upon the date on which the qualified beneficiary first becomes covered under the other group health plan (even if the other coverage is less valuable to the qualified beneficiary). By contrast, if a qualified beneficiary first becomes covered under another group health plan on or before the date on which COBRA continuation coverage is elected, then the other coverage cannot be a basis for terminating the qualified beneficiary’s COBRA continuation coverage.

(b) The requirement of this paragraph (b) is satisfied if the qualified beneficiary is actually covered, rather than merely eligible to be covered, under the other group health plan.

Treas. Reg. §54.4980B-7, Q/A-3:

**Q-. 3. **When may a plan terminate a qualified beneficiary’s COBRA continuation coverage due to the qualified beneficiary’s entitlement to Medicare benefits?

**A-3. **(a) If a qualified beneficiary first becomes entitled to Medicare benefits under Title XVIII of the Social Security Act (42 U.S.C. 1395-1395ggg) after the date on which COBRA continuation coverage is elected for the qualified beneficiary, then the plan may terminate the qualified beneficiary’s COBRA continuation coverage upon the date on which the qualified beneficiary becomes so entitled. By contrast, if a qualified beneficiary first becomes entitled to Medicare benefits on or before the date that COBRA continuation coverage is elected, then the qualified beneficiary’s entitlement to Medicare benefits cannot be a basis for terminating the qualified beneficiary’s COBRA continuation coverage.

(b) A qualified beneficiary becomes entitled to Medicare benefits upon the effective date of enrollment in either part A or B, whichever occurs earlier. Thus, merely being eligible to enroll in Medicare does not constitute being entitled to Medicare benefits.

Geissal v. Moore. Med. Corp., 524 U.S. 74 (1998):

Moore’s reading, however, will not square with the text. Subsection 1162(2)(D)(i) does not provide that the employer is excused if the beneficiary “is” covered or “remains” covered on or after the date of the election. Nothing in § 1162(2)(D)(i) says anything about the hierarchy of policy obligations, or otherwise suggests that it might matter whether the coverage of another group health plan is primary. So far as this case is concerned, what is crucial is that § 1162(2)(D)(i) does not speak in terms of “coverage” that might exist or continue; it speaks in terms of an event, the event of “becoming covered.” This event is significant only if it occurs, and “first” occurs, at a time “after the date of the election.” It is undisputed that both before and after James Geissal elected COBRA continuation coverage he was continuously a beneficiary of TWA’s group health plan. Because he was thus covered before he made his COBRA election, and so did not “first become” covered under the TWA plan after the date of election, Moore could not cut off his COBRA coverage under the plain meaning of § 1162(2)(D)(i).

Qualifying COBRA Events

Early Loss of COBRA

COBRA and Medicare

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn